Creative Ways to Get Funding

- Completion time About 25 minutes

All startups have one thing in common – they need money to get off the ground. As the saying goes, money makes the world go ‘round, and it’s extra true for small businesses. You know you need capital to get your new venture going, but where are you gonna get it?

When it comes to startup funding, you have a few options. Each of them comes with a laundry list of pros and cons, and there’s no single, right answer for everyone. In this session, we’ll work through each of the alternatives, do’s and don'ts, and dispel some common funding myths.

Options

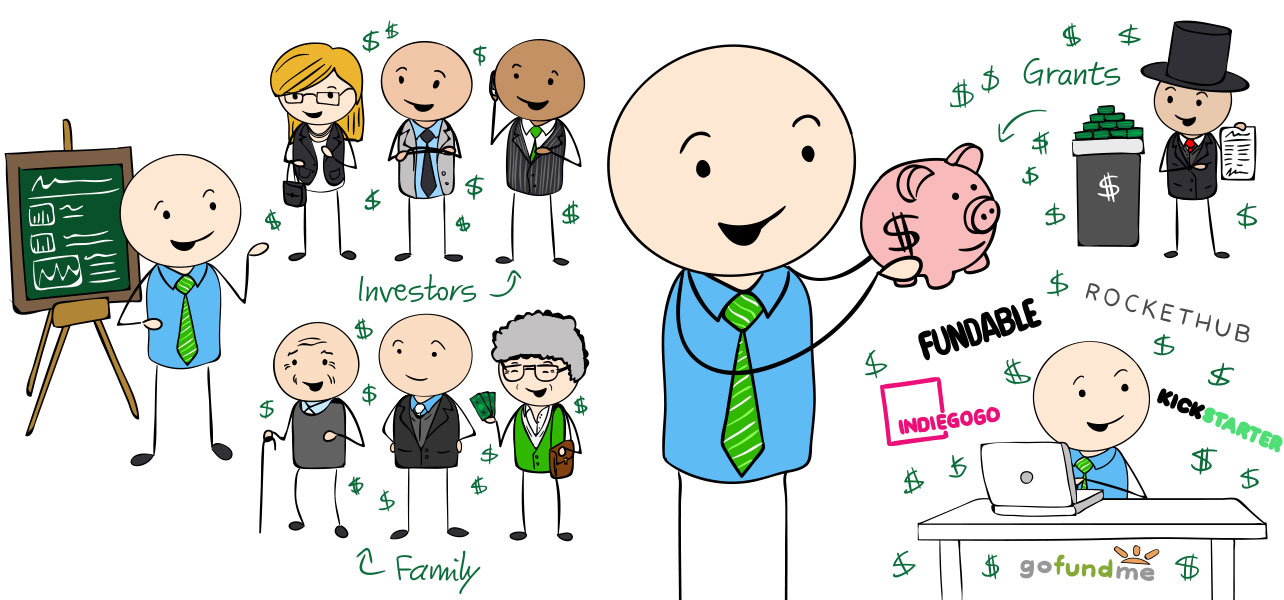

There are six main options for startup funding: bootstrapping, friends & family, crowdfunding, startup competitions & grants, loans, and angel investors & venture capitalists. Which option is best for you will depend on your funding needs, the type of business you’re in, and a lot of personal preference.

You’ll want to do thorough research to ensure you’re picking the funding method that will work best for you and your business in the long run. To start, we’ll discuss pros and cons of each, as well as some next steps to get going.

Bootstrapping

Bootstrapping is essentially just self-funding – you use your own capital to get the business going. This method has been growing during recent years, particularly because the costs to start a new business are lower than ever. As many as 82% of today’s startups are self-funded.

Pros

- You don’t give up any equity or creative control

- Your only stakeholders are your customers and your team

- Limited capital can force you to find creative solutions

- Well-suited to businesses with exceptionally low startup costs

- When profits come, they’re entirely yours

Cons

- A dip in revenue limits what you can do

- You lose out on the partnership & additional knowledge an investor might bring

- Self-funded startups can seem less credible

- More personal risk because you’re putting up your own money

- Growth can be slow without a large influx of capital

Where to Start

Step 1: Do your research, crunch the numbers, and decide how much risk you’re comfortable with. Bootstrapping doesn’t mean you have to empty your entire life savings. You can, or you can get started with a lesser amount that you’re more comfortable risking.

Step 2: Talk to entrepreneurs who’ve done it. Find out what worked for them, what didn’t, and the advice they’ve picked up along the way. You can find fellow small biz owners through your local SCORE or Chamber of Commerce, as well as online.

Step 3: Before you take the leap, consider starting your business as a side gig. You’ll keep the cash flowing in from your day job while you test your product and conduct the due diligence to ensure your idea can be successful.

Friends and Family

If bootstrapping just isn’t producing the kind of capital you need, you can sometimes turn to family and friends to help fund your startup. They know your passion and your drive, so there’s no one in the world more ready to support you.

Pros

- Most of the time, you won’t have to give up any equity or control

- Those close to you are the most likely to be supportive

- Loved ones may be as brutally honest as any investor

- You’ll be more responsible with family money than investor money

- When you pay them back, you probably won’t have to worry about interest

Cons

- Money complicates relationships

- The amount you can raise is still relatively limited

- Pressure to make changes may come from a less business-savvy source

- Some family members may feel they can’t say no

- Depending on the amount of the loan, there can be complex tax implications for both you and the lender

Where to Start

Step 1: Weigh the pros and cons. Take into consideration both the tangible and intangible consequences of accepting money from family & friends (e.g. complicating relationships, blurring the work/life line, tax implications, etc.)

Step 2: Design a pitch specifically for your loved ones. Stay away from any business-speak they may not be familiar with, be reasonable with your ask, and don’t try to hard sell your family. The arrangement can quickly turn ugly if people feel bullied into giving you money.

Step 3: Take your idea to the audience. Do everything you can to make them as comfortable as possible – encourage loved ones to ask for clarification, avoid making them feel any pressure to put up money, and be open to getting nonmonetary help

Crowdfunding

Crowdfunding is basically taking the friends & family concept to a mass audience. You’ll collect donations, presales, loans, and/or investment from anyone on the internet. Crowdfunding is relatively new and still evolving, but it’s popularity has exploded in recent years.

Pros

- You can raise more – sometimes much more – money than through family

- Different sites cater to various types of projects, leading to the most engaged audience

- Diversity means you choose whether to accept donations, presales, loans, or investment

- The funding process can be a good indicator of market interest

- You can establish an initial customer base through your campaign

Cons

- While it’s growing, you probably won’t be raising a ton of capital

- Can require you to give up some equity in the business

- Some sites require you to do all-or-nothing funding – meaning if you don’t hit your funding goal, you get nothing

- If funding is successful, a whole team of “investors” will be pushing you for results

- Posting your business idea online leaves you vulnerable to theft

Where to Start

Step 1: Determine what your funding needs are. If they’re super high or low, you may have better options than crowdfunding. Decide what kind of funding you’ll do – do you want to accept donations, presales, loans, investments, or a combination?

Step 2: Research the different sites you can use, including:

Take into consideration your funding needs, the nature of your project, and what kind of funding you want to do to determine which platform will work best for you.

Step 3: Set about creating a campaign. Do plenty of research on who your audience is and what will speak to them. Then craft a pitch that will entice people to put up their own money. Remember – you can do more than one round of crowdfunding, so take note of any key lessons.

Startup Competitions and Grants

You probably won’t be funding your entire venture through competition prize money, but there are a ton of competitions and grants offering up some notable cash. Startups competitions also give you access to in-kind prizes, critiques of your pitch or business plan, and free publicity.

Pros

- Innovative tech ventures do particularly well in this space

- You can do pretty well with nothing but a good pitch and a charismatic smile

- Grants are as close to free money as you can get

- Even if you don’t win, you’ve gotten vital publicity

- Judges can offer valuable critique of your pitch & business plan

Cons

- Competition for federal grants is incredibly fierce

- You’ll have to devote time & energy into applications and presentations

- Presenting your idea to a large audience makes you vulnerable

- Applying for a small business grant is an arduous process

- Certain types of projects won’t do as well as others

Where to Start

Step 1: Decide whether you want to pursue a startup competition or a small business grant. You can find out about startup competitions in our guide and search federal grants here. Do some research to see which competitions or grants fit well with your business.

Step 2: Get started with the necessary due diligence. If you choose a competition, research the application process and perfect your pitch and business plan. For grants – especially federal grants – the application process can be extensive, so it’s best to get a head start.

Step 3: Remember, competition is tough for both startup competitions and small business grants – don’t be discouraged if you don’t get the first one you apply for. Keep plugging away and success will happen.

Loans

Loans are pretty common among startups with up to 41% of small businesses funded through this method. The primary drawback is that you’re incurring debt, which you’ll eventually have to pay off. But if you’re willing to take the risk, a small business loan is a great option.

Pros

- You can get much more capital than through the previous methods

- You won’t usually be giving up any equity

- Banks will generally stay out of your business affairs

- Most small business loans come with reasonable interest rates & terms

- There can be tax benefits to both principal and interest payments

Cons

- Many banks will want to see a successful business track record

- If you have poor credit, lenders will be less likely to take a chance on you

- The application process can be extensive and time-consuming

- Banks are still a little tight with their wallets following the recession

Where to Start

Step 1: As always, do some research. Take a look at several banks and other lending institutions to determine which has the best terms, interest rates, etc. These can vary greatly between institutions so it’s important to research more than a few options.

Step 2: Reach out to one or a few lenders that look promising and find out what it takes to apply. If you need a business plan, ask what specifically to include. You can even ask about what kinds of businesses they’ve lent to.

Step 3: Set about preparing for the application process. If you don’t have a business plan, write one. If you do, perfect it. Craft your pitch and elevator pitch, and practice in front of an audience. Do everything you can to be as prepared as possible when the time comes.

Angel Investors and Venture Capitalists

It’s simple – VCs provide a sizable sum of capital in exchange for an (also sizable) chunk of equity. While these two methods are less common – fewer than 1% of startups secure venture investment – it can be a great option if you need a large amount of money to get going.

Pros

- You can secure a large(r) amount of capital

- Investors and VCs can lend credibility to your startup

- You’ll gain an experienced business advisor and partner

- You’ll get access to a larger network of connections

- Your business can scale quickly and efficiently

Cons

- You’ll almost definitely have to cede some equity to the investor

- VCs are the most hands-on investors and will want to influence decisions

- Investment money is incredibly competitive

- Many investors want to see proof of concept before putting up money

- You may have less discipline when it comes to spending

Where to Start

Step 1: Do your research, then do some more. The biggest threat to venture capital is when you and your investor have misaligned goals. There are enough options when it comes to investors that you can afford to be picky until you find someone who believes in your vision.

Step 2: Consider launching your business before approaching investors. If you can show sales, paying customers, and profits before you get seed capital, investors will be much more willing to fork over their own money.

Step 3: Get prepared. Perfect your business plan, crunch your numbers, and practice your pitch until it’s flawless. The key with investors is to be straightforward and compelling. They’re experienced enough to see through BS, and you need to earn their trust to get at their wallets.

Do's

Keeping a few simple best practices in mind during your funding search can streamline the process and ensure the best possible result for you and your business. Do…

- Lots of research. I mean lots. Particularly when it comes to taking investments or getting a loan, there’s really no going back, so it’s absolutely key to do as much research as possible, so you can make the most informed and knowledgeable decision.

- Take your time. Once again, you can’t always go back, so it’s important not to rush into a decision. When you’re excited about your idea, it can be tempting to gloss over the details. But getting funding right will secure your business for the future.

- Say no. You can’t be afraid to turn down deals that aren’t right for your business. Whether investors approach you or you’re not comfortable with the terms of a deal, you can always renegotiate or just say no.

- Talk to people. Don’t be afraid to reach out and ask for advice. Other entrepreneurs have been in your shoes, and they can offer valuable insight. You can never have too much information about your options.

Don'ts

Likewise, there are a few things you should steer clear of in order to be as successful as possible throughout the funding process. Don’t…

- Be unrealistic or overly optimistic. When you’re talking to investors, lenders, loved ones, or crowdfunders, presenting numbers and projections that are unrealistic makes it seem like you’re trying to trick them or worse, that you’re out of touch with reality.

- Ask for more than you need. Funding your business is a delicate balance. When you’re working in equity, debt, and capital, you don’t want to complicate things. It’s also important to be transparent about how you’re spending other people’s money.

- Jump on the first offer. The first offer you get, from the first bank or investor you talk to, isn’t necessarily going to be the best. You have other options, so there’s no reason to settle. Plus, investors are often open to negotiating, so don’t be afraid to counter.

- Overcomplicate the process. With all of the consideration that goes into a funding decision, it can be easy to get lost in complexities. Don’t. Use the information you have to make the best decision you can.

Common Funding Myths Debunked

With all that’s said and written about startup funding, there are some common misconceptions and myths that have evolved. In this section we’ll debunk some of the most prevalent myths, and tell you the real story.

Getting Funded = Success

Many founders think that money will magically build a successful company by itself. Not so. The truth is that money is a tool. When it’s wielded correctly – and combined with a good product, great strategy, and dedicated team – it can help a capable startup make things happen.

All Investors Have Your Company's Best Interest At Heart

There are plenty of investors and venture capitalists who truly want to help you build a winning business, but some are only interested in the pay day. These people will often ask for a huge chunk of equity or restrictive royalty deals. Ample research can help you avoid these guys.

Federal Grants Are "Free Money"

It’s true that federal grants don’t have to be paid back, but they do come with limitations. If you’re issued a grant for a specific purpose, you won’t have the flexibility to pivot if that idea doesn’t work out.

You Need Perfect Credit To Get A Small Business Loan

Having good credit will certainly help you get an SBA loan, but it’s not the only factor that lenders care about. If you have a winning business plan and a killer pitch, you can still get a loan with less than perfect credit (you may have to put up additional collateral to compensate).

Banks Are The Only Place To Get A Loan

Just because a bank has turned you down for a small business loan, doesn’t mean you’re out of luck. You can also look to the Small Business Administration, credit unions, and individuals or small companies.

Conclusion

There’s no one right answer when it comes to startup funding. By now, you should have a grasp on which method(s) is right for you and your business. Now it’s time to take what you’ve learned and get that money.

Here are a few resources to help you along the way:

- How to Pick a Startup Funding Strategy | Grasshopper

- More Than 15 Small Business Funding Resources for You | Small Biz Trends

- How to Get Investors and Funding for Your Business | Grasshopper

- Explore Loans, Grants & Funding | Small Business Administration

- Business Equity for Entrepreneurs | Grasshopper

- Access Government Financing | BusinessUSA

- Share this lesson

-

Talk about this lesson